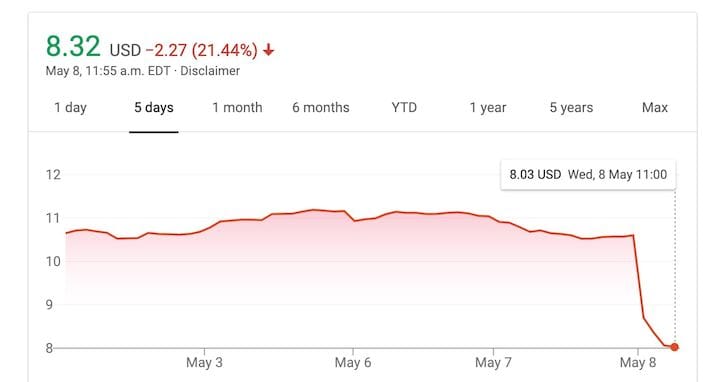

![3D Systems’ stock price dropped over 20%! [Source: Google]](https://fabbaloo.com/wp-content/uploads/2020/05/image-asset_img_5eb097e84d5d7.jpg)

3D Systems announced their quarterly results and they were not as expected.

3D Systems is one of the very few publicly-traded 3D printer manufacturers, and is one of the original inventors of 3D printing technologies, specifically the SLA process. Over the past few years their stock price has suffered as a result of the crash of interest in consumer-based 3D printing, an area where 3D Systems had invested heavily.

Since then they’ve repositioned, reorganized and reinvented themselves into a new form that was hoped to become profitable. However, that is not the case in the latest report.

Where do we start? There were quite a number of bad signals in their latest filing:

-

The first quarter revenue as compared to last year is down a massive 8% to US$152M

-

The per-share loss increased to US$0.22

-

Healthcare revenue, a major strategy for 3D Systems, declined 5%

-

Materials revenue decreased 3%

-

Software revenue decreased 8%

-

On-demand services revenue decreased 12%

-

Gross profit margins decreased by 4.7%

Was there anything positive to report? Their unit sales of 3D printers increased by a huge 90%, almost doubling their unit sales. However, this was not reflected in their revenue totals, suggesting that the machines they’re selling are of lower value than usual.

This could also suggest they are facing considerable competition for higher-end equipment from others, causing them to lower pricing.

Another positive sign was another decrease in operating expenses, which they reduced by 9%.

Generally, this is all bad news for 3D Systems.

In the past many of the publicly-traded 3D printer manufacturers have suffered quarterly losses, but they’ve been resolved by funding from large accumulated piles of cash from previous years’ profits. 3D Systems’ competitor, Stratasys, is in that boat, and they have many years of cash to burn if they continue to incur losses. This allows them considerable time to re-invent themselves.

But does 3D Systems? Their report says they have US$153.7M in cash reserves, but if the continue to lose US$24M per quarter, as has happened in this quarter, they could be in for serious troubles in the future.

Let’s compute their burn time, which is an assumption of holding the loss rate and servicing it from reserves. At this rate and level of reserves, they would have about 6 quarters of funding left, or about a year and a half.

To me, that date is dangerously near, and shows how critical it is that 3D Systems regain their profitability. Thus it is not surprising that their stock is down over 20% as of this writing.

Via 3D Systems

A blog post reveals much of what happens behind the scenes at 3D print service Shapeways.